How to Renounce U.S. Tax Residency Legally in 2026

To renounce U.S. tax residency legally is a formal act governed by IRS rules, requiring you to file Form 8854, certify five years of tax compliance, and determine whether the expatriation exit tax applies to your situation. The process is not simply a matter of moving abroad and stopping your filings. The U.S. taxes its citizens and permanent residents on worldwide income regardless of where they live, so ending that obligation requires deliberate legal steps. As of april 2026, the renunciation fee dropped from $2,350 to $450, making the process more accessible than ever before.

What are the criteria for becoming a covered expatriate subject to U.S. exit tax?

A "covered expatriate" is the IRS designation that determines whether you owe exit tax when you terminate U.S. tax residency. Covered expatriate status is triggered by meeting any one of three tests. Failing even one test places you in this category, which carries significant tax consequences.

The three tests are:

- Net worth test: Your total net worth equals $2 million or more on the date of expatriation.

- Average annual net income tax liability test: Your average annual net income tax liability exceeded $206,000 over the five years before expatriation.

- Five-year compliance certification test: You cannot certify that you have fully complied with all U.S. federal tax obligations for the five years preceding expatriation.

The net worth and income thresholds are the most straightforward to evaluate. The compliance test is where many people trip up, because it requires a clean record across all five prior years, including foreign bank account reports (FBARs) and any foreign income disclosures.

If you are classified as a covered expatriate, the IRS treats your worldwide assets as if they were sold on the day before your expatriation date. You owe capital gains tax on the resulting unrealized gains. The 2026 exclusion on those unrealized gains is $910,000, which means gains below that threshold are not taxed. That exclusion is meaningful for many middle-income expatriates, but it does not help if your portfolio is substantially larger.

Pro Tip: Run a net worth calculation at least 12 months before you plan to renounce. If you are close to the $2 million threshold, timing asset sales or restructuring holdings in advance can keep you below it.

Most Americans who renounce are not subject to exit tax at all. If your net worth stays under $2 million, your average tax liability stays under the threshold, and your returns were properly filed, the only real costs are the $450 fee and final-year tax preparation.

How to file IRS Form 8854 and your final tax returns

Form 8854 is the IRS document that formally certifies your expatriation and closes out your U.S. tax obligations. Without it, the IRS does not recognize your departure as complete. Filing Form 8854 alongside your final tax return certifies five years of compliance and reports any exit tax owed.

Follow these steps to complete the process correctly:

- Gather five years of tax records. Collect all prior federal returns, FBAR filings, and foreign income disclosures. Any gap in this record will affect your compliance certification.

- File any missing or amended returns. Correct your record before you file Form 8854. Submitting the form with known deficiencies accelerates covered expatriate classification.

- Complete Form 8854, Part I. This section confirms your personal information and expatriation date, which is the date a consular officer approves your oath of renunciation.

- Complete Part II for covered expatriates. If you meet any of the three tests, report all assets at fair market value as of the day before expatriation and calculate the taxable gain above the $910,000 exclusion.

- File with your final Form 1040. Submit Form 8854 by the same deadline as your final individual income tax return, typically April 15 of the year following expatriation.

Failure to file Form 8854, or filing it incompletely, results in automatic covered expatriate classification. That classification triggers exit tax liability and continuing annual filing obligations, even after you have left the country. The IRS does not grant exceptions for honest mistakes on this form.

Pro Tip: Work with a cross-border tax attorney or CPA who specializes in expatriation. General tax preparers often miss the nuances of Form 8854, particularly the asset valuation requirements for covered expatriates.

Tax attorney reviewing IRS tax forms at desk

Tax attorney reviewing IRS tax forms at deskReviewing common filing mistakes non-residents make before you submit your final return is a practical way to catch errors that could cost you significantly.

Steps to legally renounce U.S. citizenship and tax residency

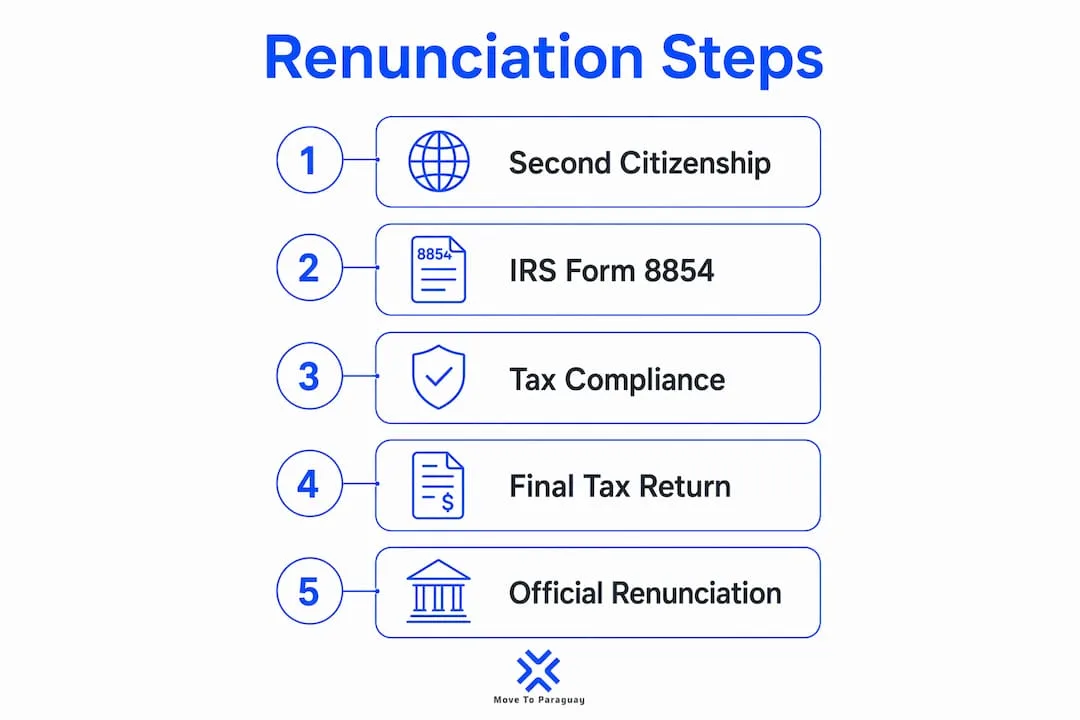

Renouncing U.S. citizenship is the most complete form of tax residency termination. The expatriation date is the date a consular officer approves your oath of renunciation, and that date legally ends both your citizenship and your U.S. tax residency.

The procedural steps are:

- Obtain a second citizenship first. The U.S. State Department requires you to hold citizenship in another country before renouncing. Without it, you would become stateless, which is not permitted.

- Schedule your first embassy interview. Contact the U.S. embassy or consulate in your country of residence. This initial appointment covers your intent and eligibility.

- Attend a second interview, spaced at least two weeks later. The two-interview process gives the consular officer time to confirm your decision is voluntary and informed.

- Pay the $450 renunciation fee. As of april 13, 2026, this fee dropped 81% from the previous $2,350. Payment is made at the consulate.

- Take the oath of renunciation. This is the formal legal act. The consular officer records the date, which becomes your official expatriation date for IRS purposes.

- Receive your Certificate of Loss of Nationality (CLN). Processing typically takes several months. The CLN is your legal proof of renunciation and is required for closing U.S. bank accounts and updating foreign financial institutions.

| Step | Document Required | Estimated Timeline |

|---|

| Second citizenship | Foreign passport | Before scheduling |

| First embassy interview | U.S. passport, foreign passport | Weeks to months for appointment |

| Second embassy interview | Same as above | 2+ weeks after first |

| Fee payment | $450 at consulate | At second interview |

| Certificate of Loss of Nationality | Issued by State Department | Several months post-oath |

Common pitfalls in renouncing U.S. tax residency

Infographic outlining legal renunciation steps

Infographic outlining legal renunciation stepsThe most expensive mistakes in tax residency termination come from misunderstanding what actually ends your U.S. tax obligations. Physical departure from the United States does not terminate tax residency for green card holders or citizens.

Green card holders maintain U.S. tax residency until they formally surrender their status using Form I-407 filed with USCIS, or through administrative or judicial termination. Simply living abroad for years while holding a green card keeps you fully subject to U.S. worldwide income tax. Many people discover this only when they face back taxes, penalties, and interest.

A single missed FBAR filing or one late tax return can convert a straightforward, low-cost renunciation into a covered expatriate event. The IRS does not weigh intent. If your five-year compliance record has a gap, you fail the certification test automatically, regardless of your net worth or income level.

Other common pitfalls include:

- Assuming departure ends tax residency. It does not. You must complete the formal legal process.

- Failing to file FBARs. Foreign bank account reports are separate from your tax return. Missing them counts as a compliance failure.

- Undervaluing assets on Form 8854. The IRS can audit asset valuations. Underreporting creates penalties on top of exit tax.

- Missing the Form 8854 deadline. Late filing results in automatic covered expatriate status.

- Not addressing prior non-compliance before renouncing. The IRS Streamlined Filing Compliance Procedures exist specifically to help expats correct prior filing failures before they renounce.

Need personalized help?

Get expert guidance for your Paraguay relocation journey. Our team is here to help you with residency, business setup, real estate, and banking solutions.

Understanding tax resident vs. nonresident rules before you begin the process prevents the most costly surprises.

Legal strategies to minimize or avoid the exit tax

Financial modeling before renunciation is the single most effective way to reduce or eliminate exit tax exposure. Advance planning can help many people avoid paying exit tax altogether, and the process is far less complex than most people expect.

- Model your net worth 12–18 months out. Calculate your total assets and liabilities now. If you are near the $2 million threshold, you have time to restructure before your expatriation date.

- Remediate prior compliance issues. Use the IRS Streamlined Filing Compliance Procedures or Voluntary Disclosure Program to correct missed returns and FBARs before filing Form 8854. Clean compliance history removes the third test as a risk entirely.

- Use the $910,000 exclusion strategically. If you are a covered expatriate, sequence asset sales to maximize the exclusion. Assets with the highest unrealized gains should be evaluated first.

- Time your renunciation relative to income and asset values. Renouncing in a year when your portfolio is down or after a major asset sale reduces the taxable gain the IRS calculates on your deemed-sale date.

- Consult a cross-border tax attorney before scheduling your embassy appointment. The expatriation date is fixed once set. There is no going back to adjust your tax position after the oath is taken.

Avoiding costly LLC mistakes is also relevant if you hold U.S. business interests, since those assets factor directly into your net worth calculation and exit tax exposure.

Pro Tip: The exit tax is feared far more than it deserves to be. Most Americans who renounce do not owe it. The key is filing accurately and planning early, not avoiding the process out of fear.

Key Takeaways

Legally terminating U.S. tax residency requires completing Form 8854, certifying five years of IRS compliance, and addressing exit tax exposure before your expatriation date is set.

| Point | Details |

|---|

| Covered expatriate triggers | Meeting any one of three IRS tests: net worth over $2M, average tax over $206,000, or failed compliance certification. |

| Form 8854 is mandatory | Filing it with your final return certifies compliance; missing it causes automatic covered expatriate status. |

| Fee reduction in 2026 | The renunciation fee dropped from $2,350 to $450 as of april 13, 2026. |

| Green card holders must act formally | Physical departure does not end tax residency; Form I-407 is required to surrender green card status. |

| Planning eliminates most exit tax risk | Most Americans who renounce owe no exit tax if they file accurately and plan their finances in advance. |

What I have learned after guiding clients through renunciation

The single biggest misconception I see is that renunciation is primarily an emotional decision. People agonize over the symbolism of giving up their passport while underestimating the technical precision the IRS requires. The paperwork is what determines your financial outcome, not the sentiment.

What I have found is that clients who come in 18 months before they want to renounce almost always have better outcomes than those who come in 60 days before. The earlier group has time to fix compliance gaps, revalue assets, and time their expatriation date strategically. The later group is often forced to accept covered expatriate status because there is no time to remediate.

The irreversibility of renunciation also deserves more weight than most guides give it. Once the consular officer records your oath, that date is fixed. You cannot retroactively adjust your asset values, file missing returns, or change your mind about the timing. Preparation is not optional. It is the entire game.

My honest advice: treat the compliance review as the most important step, not the embassy appointment. The appointment is a formality. The five years of tax records you bring to it determine everything.

— Alejandro

How Movetoparaguay supports your tax residency transition

Relocating abroad while managing IRS compliance is a process that rewards preparation and penalizes guesswork.

Movetoparaguay works with U.S. expats and remote workers who are ready to exit U.S. tax residency and establish legal residency in Paraguay. Paraguay operates on a territorial tax system, which generally means 0% tax on foreign-source income. That structure makes it one of the most practical destinations for Americans seeking a clean, compliant break from U.S. worldwide taxation. Movetoparaguay offers tailored consultations that review your specific financial situation, guide you through Form 8854 preparation, and support your residency application from start to finish. Visit Movetoparaguay to schedule your consultation and get a clear picture of your next steps.

FAQ

What does it mean to renounce U.S. tax residency legally?

Legally terminating U.S. tax residency means completing the formal IRS expatriation process, including filing Form 8854 and certifying five years of tax compliance. For citizens, it also requires renouncing citizenship at a U.S. embassy or consulate.

Who qualifies as a covered expatriate?

A covered expatriate is anyone who meets at least one of three IRS tests: net worth of $2 million or more, average annual tax liability above $206,000 over five years, or failure to certify full tax compliance for the prior five years.

Does leaving the U.S. automatically end my tax residency?

No. Physical departure does not end U.S. tax residency for citizens or green card holders. Green card holders must formally surrender their status using Form I-407 filed with USCIS.

What is the exit tax and how much will I owe?

The exit tax treats your worldwide assets as sold on the day before expatriation. Covered expatriates pay capital gains tax on unrealized gains above the 2026 exclusion of $910,000. Most Americans who renounce owe no exit tax if their finances are below the covered expatriate thresholds.

How much does it cost to renounce U.S. citizenship in 2026?

The renunciation fee is $450 as of april 13, 2026, down from $2,350. Additional costs include final-year tax preparation and, if applicable, exit tax on unrealized gains above $910,000.