What Is Tax Residency in Paraguay? 2026 Guide

Tax residency in Paraguay is defined as your formal status as a taxpayer registered with Paraguay's national tax authority, the Dirección Nacional de Ingresos Tributarios (DNIT), with verified local economic activity. This status is separate from immigration residency, and understanding the difference is the first thing you need to get right before relocating. Paraguay's territorial tax system taxes only income earned inside the country, which means your foreign income is generally exempt from Paraguayan taxation. For families and individuals planning a move, knowing what is tax residency Paraguay requires, and how to establish it properly, determines how much you pay and where.

What is tax residency in Paraguay?

Tax residency in Paraguay is established through registration with DNIT and proof of local economic activity, not through counting days on a calendar. This distinction matters because many people assume that simply living in Paraguay long enough makes them a tax resident. It does not.

The legal framework governing tax residency comes from Law No. 6,380/2019 and its implementing Decree No. 3,181/19. These laws define the criteria for tax domicile and the obligations that follow. The key elements DNIT looks for are:

- RUC registration: The Registro Único del Contribuyente (RUC) is Paraguay's unique taxpayer registry number. You cannot legally issue invoices or file taxes without it.

- Cédula de identidad: Your Paraguayan national identity card is required to obtain the RUC. You get the Cédula after securing at least temporary residency.

- Verifiable local economic activity: DNIT requires evidence that you participate in Paraguay's economy, such as invoiced transactions, a registered business, or declared local income.

- Tax compliance history: Consistent filing and payment records with DNIT strengthen your tax residency standing.

The 120-day rule is widely misunderstood. DNIT uses it only as a fallback tool to assign domicile when a taxpayer's declarations appear unreliable. It is not a legal requirement to obtain or maintain tax residency. You do not need to spend 120 days per year in Paraguay to qualify.

Pro Tip: Get your RUC registered as soon as you receive your Cédula. Delays in RUC registration push back your entire tax residency timeline, including your ability to obtain the official tax residency certificate.

Expat reviewing RUC registration documents at a DNIT office in Paraguay

Expat reviewing RUC registration documents at a DNIT office in ParaguayHow Paraguay's territorial tax system works for residents

Paraguay operates a pure territorial tax system, meaning only income generated inside Paraguay is subject to local taxation. Income you earn from clients, investments, or businesses located outside Paraguay is not taxed by DNIT. This is the core financial benefit that draws U.S. expats, remote workers, and international investors to the country.

The tax rates that apply to local income are low and flat. The table below summarizes the main rates:

| Tax Type | Rate | Applies To |

|---|

| Personal income tax (IRP) | 10% | Paraguayan-source personal income |

| Corporate income tax (IRE) | 10% | Business profits from local activity |

| IRE SIMPLE regime | 3% | Small businesses with simplified filing |

| Value-added tax (VAT) | 10% (5% on some goods) | Local goods and services |

| Wealth tax | None | Not applicable in Paraguay |

| Foreign income tax | None | Exempt under territorial system |

Overview of Paraguay's territorial tax rates for residents and expats in 2026

Overview of Paraguay's territorial tax rates for residents and expats in 2026Paraguay also lacks wealth tax, net-worth tax, and annual asset declarations on foreign assets. Property taxes are low. This structure makes Paraguay one of the most tax-efficient jurisdictions in Latin America for individuals with significant foreign income.

Once you hold tax resident status, DNIT can issue you a Certificado de Residencia Fiscal, or tax residency certificate. This document proves your tax status to foreign authorities and supports treaty benefits when applicable. It is the document your home country's tax authority will ask for if you claim Paraguay as your primary tax domicile.

Pro Tip: If you earn income exclusively from outside Paraguay, your Paraguayan tax bill can be close to zero. But you still need active RUC registration and at least minimal local transactions to hold valid tax resident status and obtain the certificate.

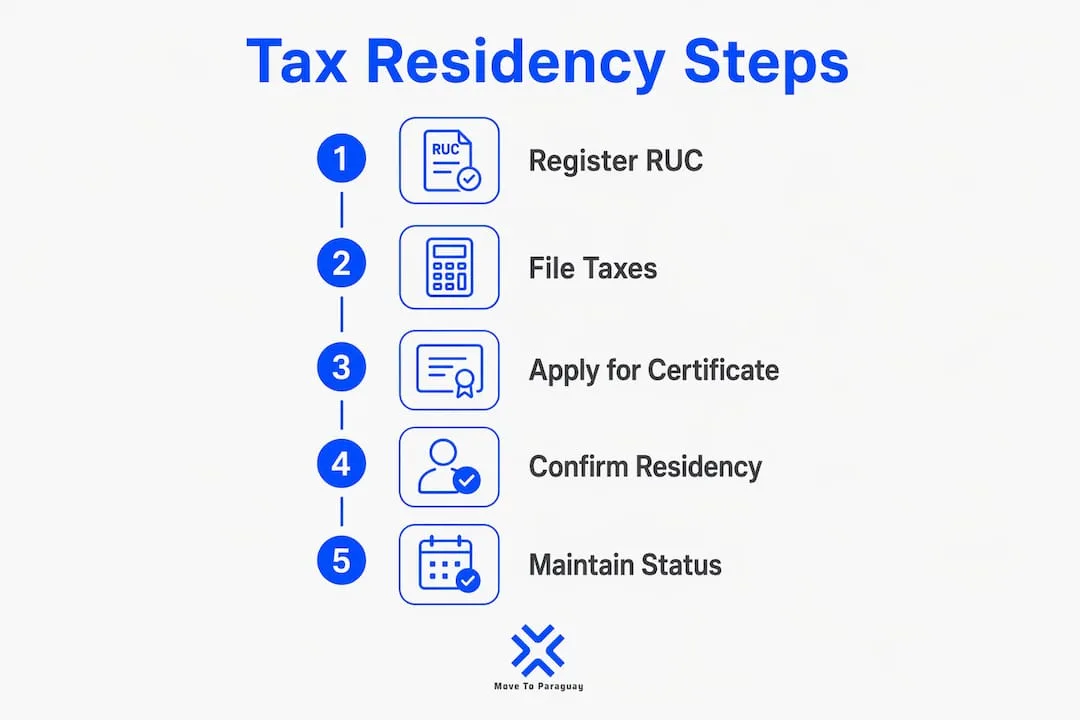

Steps to establish tax residency in Paraguay

Establishing tax domicile in Paraguay follows a clear sequence. Skipping steps creates gaps that DNIT will notice during audits or certificate requests.

- Obtain temporary residency. Temporary residency is the legal entry point. You apply through Paraguay's immigration authority, the Dirección General de Migraciones, with documents including a birth certificate, police clearance, and proof of income or investment. Processing typically takes 60–90 days.

- Collect your Cédula. After temporary residency is approved, you apply for the Paraguayan national identity card at the Departamento de Identificaciones. The Cédula is your legal identity document inside Paraguay and the prerequisite for RUC registration.

- Register for the RUC with DNIT. RUC registration formalizes your presence in Paraguay's tax system. You select a tax category based on your activity type. For most expats, the IRE SIMPLE regime at 3% is the most practical starting point.

- Generate and declare local income. DNIT requires evidence of real economic participation. Filing under the IRE SIMPLE 3% regime on even modest local transactions creates a documented tax footprint. This footprint is what makes your tax residency certificate audit-proof when presented to foreign tax authorities.

- Transition to permanent residency. After three years on temporary residency, you qualify for permanent residency. Permanent residency strengthens your tax domicile claim and removes renewal obligations. For investors, the Investor Pass pathway introduced in 2026 allows direct permanent residency without the standard $5,000 refundable bank deposit, provided you deploy qualifying capital.

- Request the Certificado de Residencia Fiscal. Once your RUC is active and your tax filings are current, you apply to DNIT for the official tax residency certificate. This certificate is the document that formally establishes your status for international purposes.

- Review double taxation agreement implications. Paraguay has Double Taxation Agreements (DTAs) with select countries. Tax residency in Paraguay does not automatically eliminate obligations in your home country. Tie-breaker rules in each DTA determine which country has primary taxing rights when you hold residency in two jurisdictions simultaneously. A qualified tax advisor should review your specific situation before you exit your home country's tax system.

For a detailed breakdown of the residency application process, the step-by-step residency guide covers both temporary and permanent pathways with current 2026 requirements.

Need personalized help?

Get expert guidance for your Paraguay relocation journey. Our team is here to help you with residency, business setup, real estate, and banking solutions.

Common misconceptions about Paraguay tax residency

The biggest mistake people make is assuming that immigration residency and tax residency are the same thing. They are legally distinct, and one does not guarantee the other. You can hold a valid Paraguayan residency permit and still not qualify as a tax resident if you have not registered with DNIT and established local economic activity.

Other frequent misconceptions include:

- "I need to spend 120 days in Paraguay to be a tax resident." False. The 120-day rule is a DNIT administrative tool, not a legal threshold. Tax residency is determined by registration and economic ties, not physical presence.

- "My foreign income will be taxed once I register." False. Paraguay's territorial system exempts foreign-source income entirely. Only income generated inside Paraguay falls under DNIT's jurisdiction.

- "I can skip RUC registration and still claim tax residency." False. Without an active RUC, you have no formal standing in Paraguay's tax system. DNIT cannot issue a tax residency certificate to someone who is not registered.

- "Permanent residency automatically makes me a tax resident." False. Permanent residency is a strong foundation, but tax residency requires separate registration steps with DNIT.

The risks of skipping formal registration are real. If your home country's tax authority challenges your claimed tax domicile, you need documented proof: an active RUC, filed returns, and the Certificado de Residencia Fiscal. Without these, your Paraguay tax residency claim will not hold up under scrutiny.

Pro Tip: Keep copies of every DNIT filing, RUC registration document, and tax payment receipt. If your home country audits your tax residency claim, this paper trail is your primary defense.

Understanding the difference between tax resident and nonresident status under Paraguayan law is the clearest way to avoid costly errors before and after your move.

Movetoparaguay: your guide to tax residency in Paraguay

Relocating and establishing tax residency involves more moving parts than most people expect. Movetoparaguay specializes in guiding U.S. expats, Brazilian nationals, and international families through every step, from the first residency application to RUC registration and ongoing tax compliance with DNIT.

Movetoparaguay offers tailored consultations that review your individual case in detail, so you receive specific next steps rather than generic advice. Services include Paraguayan company formation, tax filing under the IRE SIMPLE regime, and full support obtaining your Certificado de Residencia Fiscal. If you are ready to establish your tax residency in Paraguay with a clear plan and transparent timelines, visit Movetoparaguay.

Key Takeaways

Tax residency in Paraguay requires formal DNIT registration, an active RUC, and verifiable local economic activity. Physical presence alone does not establish tax resident status.

| Point | Details |

|---|

| Tax residency vs. immigration residency | These are legally separate; immigration status does not create tax residency with DNIT. |

| RUC is mandatory | You cannot hold valid tax resident status or obtain the tax residency certificate without an active RUC. |

| Foreign income is exempt | Paraguay's territorial system taxes only local-source income; foreign earnings face no Paraguayan tax. |

| The 120-day rule is a myth | DNIT uses it as an administrative fallback, not as a legal requirement for tax residency. |

| Certificate requires active compliance | DNIT issues the Certificado de Residencia Fiscal only after confirmed RUC registration and filed returns. |

FAQ

What is the difference between immigration and tax residency in Paraguay?

Immigration residency grants you the legal right to live in Paraguay. Tax residency requires separate registration with DNIT, an active RUC, and verified local economic activity. One does not automatically create the other.

Do I need to spend 120 days in Paraguay to become a tax resident?

No. The 120-day rule is an administrative tool DNIT uses to assign domicile when declarations are unreliable. Tax residency is established through RUC registration and local economic activity, not physical presence.

What is the RUC and why does it matter for tax residency?

The RUC is Paraguay's unique taxpayer registry number, issued by DNIT. Without it, you cannot file taxes, issue invoices, or obtain the official tax residency certificate.

Is foreign income taxed once I become a Paraguay tax resident?

No. Paraguay taxes only income generated inside the country. Foreign-source income is fully exempt under the territorial tax system, regardless of how much you earn abroad.

How do I get the official Paraguay tax residency certificate?

You apply to DNIT after your RUC is active and your tax filings are current. DNIT issues the Certificado de Residencia Fiscal as proof of your tax status for foreign authorities and treaty purposes.